On 24 September 2025 the government announced the Board of Taxation (the Board) will review ways to reduce red tape in the tax system.

Background

The government is interested in ways to reduce red tape in the tax system. Reducing red tape will help ease the compliance burden on businesses. It will also make our economy more productive.

As part of the Economic Reform Roundtable process, the Treasurer wrote to Commonwealth regulators. The Treasurer asked for actions each regulator could implement to reduce compliance burdens to support productivity.

The Commissioner of Taxation responded to the Treasurer’s request. Along with other things, the Australian Taxation Office (ATO) will develop a compliance cost framework. This framework will help the ATO understand how regulation and compliance impact taxpayers.

Terms of Reference

To complement and support the ATO’s work, the Board is requested to:

- engage with the business community to identify areas of business tax law and administration where there are opportunities for red tape reduction that are substantial, material, measurable and directly support productivity.

- Where opportunities are identified:

- If involving administrative changes, provide the examples to the ATO to support their red tape work, including indicating the benefits that may be possible from reducing compliance costs; and

- If involving legislative changes, provide recommendations to government for potential improvements. Any recommended improvements should consider the benefits to productivity, be revenue neutral and consider any potential integrity risks.

As part of the review, the Board will stocktake any tax‑related compliance and red tape reduction recommendations from the Economic Reform Roundtable public submissions, as well as previous Board reviews and recent stakeholder engagement by the Board which discussed tax compliance burden.

The Review Team

The Board has appointed the following Board Members to oversee the review:

- Andrew Mills (Acting Chair)

- Ian Kellock

- Andrea Laing

- Judy O’Connell.

They will be assisted by the Board’s Secretariat function.

Consultation

The Board will consult with a wide range of stakeholders.

Consultation will help the Board understand where the impacts of compliance and regulation on business taxpayers could possibly be reduced through changes in business tax law and administration.

The Board has prepared a consultation guide [PDF 444 KB | DOCX 227 KB] to explain the review process. The guide details the consultation process, how stakeholders can contribute and questions to consider.

Consultation sessions

Consultation sessions were held during November 2025. Thank you to those who attended a session and contributed ideas.

The Board may conduct targeted consultations as the review progresses further.

Submissions

Written submissions closed on 15 December 2025. The Board thanks those who made a submission to the review.

Progress update – March 2026

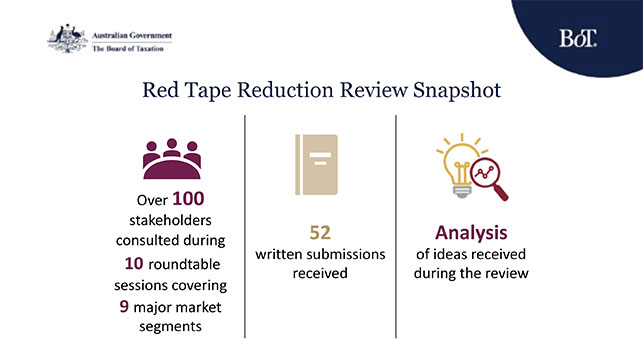

The Red Tape Reduction Review public consultation phase was held in November 2025. Written submissions were received by the end of 2025. The Board sincerely thanks everyone who took the time to provide feedback and contribute ideas.

The graphic below outlines the progress of the review.

The Board is undertaking targeted engagement with stakeholders to explore specific proposals in greater depth, seek clarification, and assess feasibility and potential impact. This further analysis will inform the development of the Board’s recommendations.

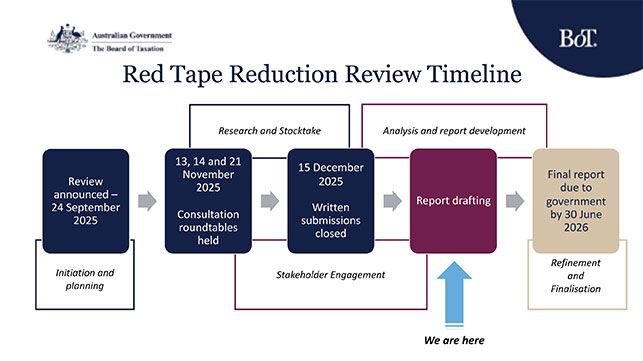

The timeline below highlights the movement through various phases of the review.

Further updates will be published as key milestones are reached.

Timing

The Board is expected to report back to Government by 30 June 2026, which is on track to be delivered on time.

More information

For more information, contact the Board of Taxation Secretariat at taxboard@taxboard.gov.au